Principal Components Regression: Recap of Part 2

Recall that the least squares solution to the multiple linear problem is given by(1) $latex \hat{\beta} = (X^T X)^{-1} X^T y $

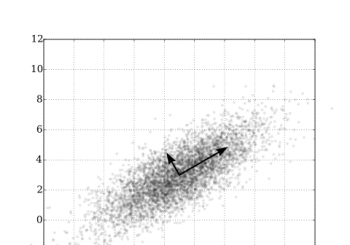

And that problems occurred finding when the matrix(2)

was close to being singular. The Principal Components Regression approach to addressing the problem is to replace in equation (1) with a better conditioned...

Read More

Read More